Redesigning the Mobile Banking Experience for India's No.1 Bank

The Team & My Role

Led end-to-end design for the project, managing a multidisciplinary team and collaborating closely with cross-functional stakeholders across the organization

Internal

- Role

- Lead Designer

- Design Team

- 5 Product Designers

- Motion & Illustration

- On-demand specialists

- Project Manager

- Delivery & Coordination

Client

- Product Team

- Requirements & Prioritisation

- Engineering Team

- Feasibility & Implementation

- Experience Design Team

- Alignment & Collaboration

- C-Suite

- Workshops & Strategic Direction

The Challenge

Bridging the gap between digital capability and modern user expectations for 12 crore users

HDFC Bank has long been a digitally progressive institution, but its mobile experience had not kept pace with evolving user expectations and advancements in the ecosystem. Key journeys presented opportunities to reduce friction, improve accessibility, and create a more cohesive, modern experience.

-

"Fragmented user base. We need to bring bank branch users and net-banking users to the mobile app. Only 50% of HDFC Bank users use the mobile app"

— Chief Digital Officer -

"There's too much friction when it comes to making transactions. Core payment functionality like recurring payments and UPI are missing"

— Product Team representative -

"Users are highly dependent on the Customer Support Team, overwhelming the support function. We need the app to be self sufficient, and more user friendly"

— Customer Support Team representative

Research & Discovery

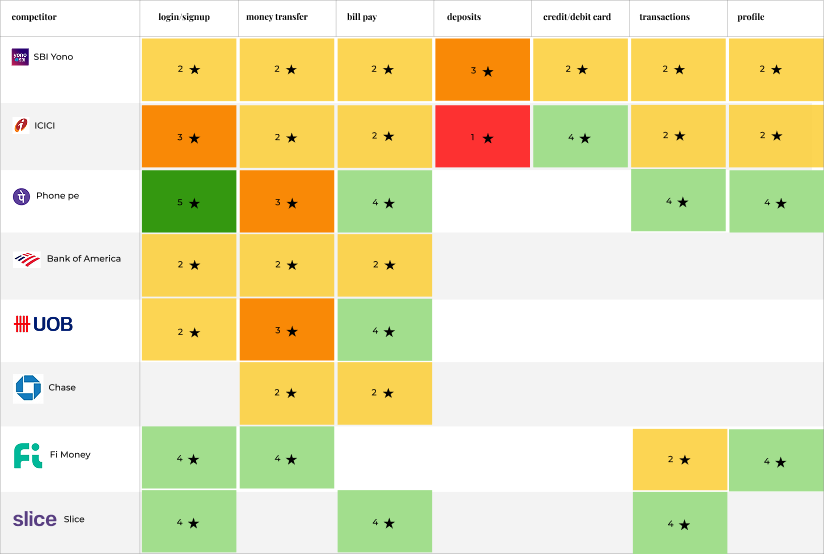

Direct user access was limited, so we triangulated insights through stakeholder interviews, workshopping, and competitive benchmarking.

- Stakeholder interviews across customer support, product, engineering, and branch operations

- Workshops with leadership to align on vision and principles

- Strategic benchmarking (best-in-class products like Airbnb, Uber)

- Tactical benchmarking (banks, fintech apps, neo-banks)

Insights

Key product and experience gaps impacting adoption

-

01

High-frequency actions like payments were not optimized for speed or accessibility, increasing reliance on alternative apps.

-

02

Users depended on customer support for basic tasks, indicating gaps in product clarity and self-sufficiency.

-

03

User segments were fragmented across channels (branch, NetBanking, mobile), limiting adoption of the app as a primary interface.

-

04

Discovery of new and existing products was limited within the app, suppressing cross-sell and engagement.

-

05

Onboarding and access flows introduced uncertainty, causing drop-offs before users experienced value.

-

06

The existing design language lacked consistency and modern appeal, impacting trust and competitiveness with fintech products.

-

07

There was a gap between HDFC's digital capabilities and how effectively those capabilities were surfaced to users.

-

08

Poor UX copy and a lack of strong brand voice led to many errors and confusion.

Constraints & Guardrails

Balancing usability with compliance, trust, and system realities

-

Regulatory Compliance

Key flows like onboarding, authentication, and data access had to meet strict regulatory requirements, limiting how much friction could be removed.

-

Security & Trust Sensitivity

Users were cautious about sharing personal and financial information, requiring clearer communication rather than reducing safeguards.

-

Existing Mental Models

Users relied on familiar banking patterns, making it important to align new interactions with established expectations.

-

System-Driven Dependencies

Backend processes such as customer data fetching and device binding constrained how certain flows could be simplified.

-

Diverse User Base

The experience needed to work across varying levels of digital literacy, requiring clarity, guidance, and reduced cognitive load.

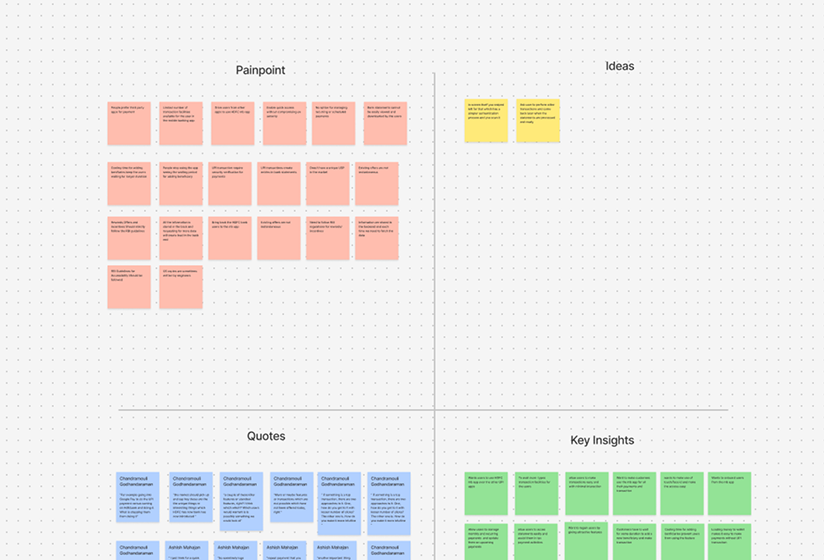

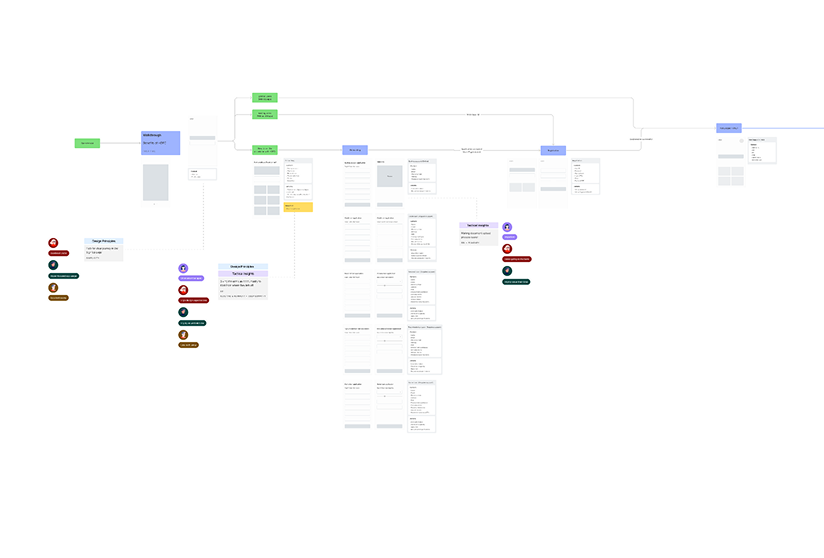

Process Artefacts

Supporting research and exploration

-

Competitive Benchmarking

-

Discovery Workshops

-

Information Architecture

Users

Designing for a diverse and fragmented user base

Through stakeholder interviews and internal research, we identified distinct user behaviors and needs across HDFC's customer base. These patterns helped us simplify complexity into clear user segments that directly informed key product decisions.

-

Digitally Active

Comfortable with fast payments and expect minimal friction

Enabled fast-access features like pre-login UPI and reduced interaction steps.

-

Low-Confidence / Assisted

Depend on support and need clarity in flows

Shaped guided onboarding, contextual help, and transparent permission flows.

-

Existing but Inactive

Already bank customers but not mobile users

Influenced multiple registration methods and inclusive access.

Strategy

Defining product bets and design principles to guide the experience

The research revealed systemic gaps across onboarding, access, and core journeys. We translated these into a set of product-level bets and guiding principles to improve activation, engagement, and long-term adoption.

Product Bets

-

Reduce friction at entry

Improve onboarding completion and activation

-

Enable self-sufficient usage

Reduce dependency on support

-

Unlock existing user base

Increase activation without new acquisition

-

Increase frequency of use

Drive engagement through faster access

-

Establish a scalable design foundation

Improve consistency and long-term usability

Design Principles

-

Deep Empathy

Design with a clear understanding of user context, constraints, and behavior — especially in high-stakes financial interactions.

-

Progressive Inclusivity

Create experiences that work across varying levels of digital familiarity, access, and confidence.

-

Positive Surprise

Introduce moments of delight within functional flows to make the experience feel engaging and human.

-

Evolve & Adapt

Continuously evolve patterns and interactions to meet changing user expectations and technological advancements.

-

Simplicity

Prioritize clarity and ease of use, reducing complexity in critical journeys to enable faster, more confident actions.

These principles guided decision-making across the entire product.